NEVER STORE MONEY

A fertile effort made by most conservative investors is the search for an excellent long-term investment. There are suitable investments, but when it comes to stocks and bonds, there are no suitable long-term investments. As inflation and interest rates change, this year’s best investment will be the worst in two or three years.

CHOOSE THE RIGHT TYPE OF FUNDS FOR EACH ECONOMY

If the secret to safely investing in stocks and bonds is the Mutual/Segregated Fund, then the secret to making money is that there are three entirely different types of funds: Stocks, Bonds and Money Market.

The “Money Movement Strategy” matches the suitable investment to the right economic climate, thereby creating an average investment return of 15%-20% per year.

INVEST IN ONLY ONE TYPE OF FUND AT A TIME

One and only one type of fund is right for each economy. But unfortunately, one major mistake made by most Financial Planners, often on the advice of their Head Office, is over-diversification.

When dividing investment capital among stocks, bonds, Government securities, and money market funds, over-diversification will cost as much in lost profits as under diversification. This is because an overly diversified investment plan operates like a seesaw; when one side goes up, the other goes down.

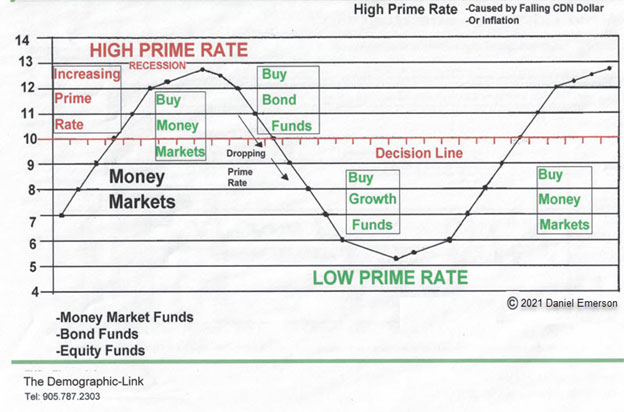

USE THE PRIME INTEREST RATE TO IDENTIFY THE SAFEST AND BEST FUND INVESTMENT FOR EACH ECONOMY

What factor identifies the current economy and, therefore, the correct investment? – INTEREST RATES – more specifically, prime interest rate. Eighty percent of the long-term increase or decrease in the value of the stock, bonds, and money market instruments is caused by changes in interest rates and is predictable. Conversely, short-term, nonpredictable increases or decreases are caused by speculation.

The prime rate is the easiest of the interest rates to follow; any changes make front-page headlines.

You must watch two components of the prime rate to choose the suitable investment:

- 1- PRIME RATE LEVEL – high or low

- 2- PRIME RATE DIRECTION – up or down

INVEST IN STOCK FUNDS ANY TIME THE PRIME RATE IS LOW

There is always one of the three types of funds – stock, bonds or money market, that will give you a positive return and average out to 15% per year or more. The prime rate indicates which one.

The investor’s Decision line does change, but only once every few years. The area below the investor’s decision line defines a Bull market when most stocks and stock funds are rising.

The big Institutional investors get into the stock market when the prime rate drops and out of the stock market when the prime rate rises.

Traditionally over 80% of stocks are owned by just three groups of Institutional investors: Mutual funds, Pension funds and big corporations. When the big guys buy, stocks go up. When the big guys sell, stocks go down.

When is the correct time to invest in stock funds? Any time the prime rate is below the investor’s Decision line. During those years, no matter how widely the markets fluctuate, the stock market and stock funds will grow an average of 15%-20% or more. Of course, during this period, there will be unpredictable corrections.

The Money-Movement Strategy allows you to react logically rather than emotionally to these corrections. Typically a slingshot follows any correction of size. On average, slingshot will regain all lost ground and move on to higher territory. A total return of 40% is common in a slingshot, so never invest emotionally. Always use logic.

MOVE YOUR MONEY TO A MONEY MARKET FUND WHEN THE PRIME RATE MOVES ABOVE THE INVESTOR’S DECISION LINE

How do you know when a bull market is really over? When the prime rate rises and reaches the investor’s decision line. At that time, move your money out of the stock funds and into Money Market funds. When the prime rate is above the investor’s decision line, Money Market funds will give you the best return and be the safest investment from the coming Bear Market in stocks and radical drops in bond prices.

MOVE YOUR MONEY TO A BOND FUND WHEN THE PRIME RATE IS HIGH AND COMING DOWN

If the prime rate is over the investor’s decision line and moving up, stay in money market funds. If the prime rate changes direction and starts downward, move your money to the third and last investment in the prime rate cycle, a Bond fund.

Bond funds are always the best investment when the prime rate is high and coming down. During that period, you will earn two profits from bonds – interest and appreciation. The appreciation can be your big profit, averaging more than 20% per year. If the prime rate drops 1%, bonds appreciate 8%.

In 1984 when I started to use this strategy, I said prime rate down “one,” bonds and bond funds up “eight.” Eight-to-one was the best leverage you’ll ever get in a safe investment plan. A good example was 1982 when the prime rate dropped 5% from 16.5% to 11.5%; an average bond fund appreciated 40%.

MONEY MOVEMENT STRATEGY SUMMARY

There is always one type of fund in which you will earn an average of 15% to 20% or more over time. In 1981 it was a money market fund. In 1982 and 1984, it was bond funds. In 1983, 1985, 1986, 1987 and 1988, the right investment was stock funds.

In November 1988, Money Market funds were investments through June 1989. Bond funds became the right investment until March 1991, when stock funds became the best investment choice.

The Money Movement Strategy will always have you at the right place at the right time and overcome the problem of short-term market drops.

The Money Movement Strategy will produce the most significant profits when the prime rate drops, often 30% or more per year in stocks or bonds.

When the prime rate rises, money movement becomes a defensive strategy, and profits are in the 5% to 10% range.

The Money Movement Strategy is not intended to be a get-rich-quick scheme. It is a lifelong strategy for reducing risk and maximizing investment profits.

The Money Movement Strategy will allow you to average 17% yearly, year after year – without having to watch your money daily. It is a winning Mutual/Segregated fund Strategy for conservative and aggressive investors. You can use this program in your TFSA, RESP, RRSP, LIRA, investment portfolio, and a 100% tax-free insurance policy.

Throughout the 1990s, over ten years using the Money Management Strategy, we averaged 24% per year, which is documented in black & white in the Bruce County Market Place Magazine in the period for our clients. I know no other advisor with that track record that has documented proof.

(This is one of the first strategies I used, starting as early as 1984. While some of this article is still very valid, the globalization of economies & markets now requires more sophisticated strategies).

Again I want to remind readers that I no longer sell Insurance or investment products; I only advise as a consultant, which I am allowed to do as I spent 35 years in the Financial service industry.